ELECTRIC INSURANCE

Snow causes a tree to collapse and damage your property

Are you covered?

Share this:

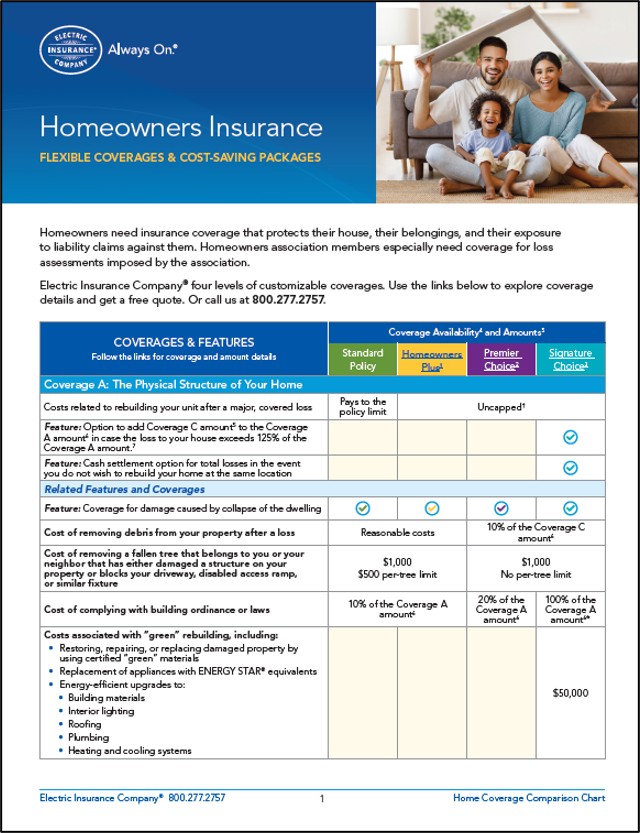

Home values are at an all-time high. Make sure you protect your investment in your home with sound coverage. This easy-to-understand coverage chart (PDF 861kb) helps you know what to get and why.