Insurance FAQs

Here's where you'll find immediate answers to some of the most common general insurance and billing, claims and coverage-related questions. Just click on any of the titles under the icons below to find information on that topic.

Most Popular Q&As

Login to MyAccount to view/print your ID cards - this short video will show you how. You can also find a copy of your ID Cards in your renewal policy packet.

In most cases, “yes.” Electric Insurance will extend the broadest insurance of any vehicle on your auto policy to any private passenger type vehicle you rent in the United States, provided the rental period does not exceed 30 days.

Our insurance would apply as excess over any other collectible source of recovery (e.g., insurance provided by a rental company, travel or accident policies, or any applicable credit card coverage).

If you have purchased Collision and Other Than Collision/Comprehensive from Electric Insurance on one of your autos, that insurance will extend to insure damage to a rented vehicle, subject to your policy deductible.

For example, if the rental agreement provides a $1,000 Collision deductible and you have purchased from Electric Insurance a $250 Collision deductible, your policy with us will pay the difference between the $250 and $1,000.

If your Electric Insurance policy does not have Collision and Other Than Collision/Comprehensive coverage, you should consider purchasing the additional insurance from the rental agency.

Your Liability coverage (Bodily Injury, Property Damage) will also apply as additional insurance over and above the liability protection provided by the rental agreement.

The answer to this question in most cases is, "yes."

Insurance coverage follows the vehicle. For example, if a neighbor or friend, someone who does not live in your household, borrows your vehicle, they may be covered under your auto policy. This would apply to an occasional, short-term situation (one month or less). This does not apply to rented vehicles; your policy’s coverage, regarding letting someone borrow your car, only applies to vehicles listed on your automobile policy.

Electric Insurance offers several convenient options for making payments.

- Sign into the MyAccount Policy Management Center to make a one-time payment or set up automatic, recurring payments from your checking or savings account or credit or debit card.

- Use the "ONE-TIME PAYMENT" button on the top menu of any page on our website.

- Pay by phone: Call our automated system any time at 844.516.4345.

- Pay by mail: Mail your check or money order to Electric Insurance Company, PO Box 9147, Chelsea MA 02150.

- Online banking (paying from your financial institution’s site): Be sure to enter your account number and the mailing address: P.O. Box 9147, Chelsea, MA 02150.

Late payments are subject to a late fee, as allowed by state regulations. If your payment is past due, you may be sent a Notice of Cancellation. If you receive a Notice of Cancellation for non-payment, please pay the amount due on the cancellation notice so that your policy will not be cancelled.

In most cases, your homeowners (or condominium unit owners or renters) policy would extend to cover your child’s property in a dorm or other residence if the student is under age 24, enrolled in school full-time, and was a resident of your household before moving out to attend school.

The coverage amount is limited to 10% of your policy’s Coverage C amount or $1,000, whichever is greater. The coverage applies to personal property anywhere in the world if the loss was caused by a covered peril. The policy deductible would apply.

You may wish to consider a separate renter’s policy for your child. If your child makes a claim under the renter’s policy, it would not adversely affect your home policy (such as removing any “claim-free” discount or adding a surcharge to your premium.) Please note that a landlord may require all renters to have a renter’s policy.

Auto Insurance

Login to MyAccount to view/print your ID cards - this short video will show you how. You can also find a copy of your ID Cards in your renewal policy packet.

Yes, your policy will renew automatically, unless we receive written notification that you intend to cancel your policy. You will receive your renewal policy packet and your bill will come separately.

The answer to this question in most cases is, "yes."

Insurance coverage follows the vehicle. For example, if a neighbor or friend, someone who does not live in your household, borrows your vehicle, they may be covered under your auto policy. This would apply to an occasional, short-term situation (one month or less). This does not apply to rented vehicles; your policy’s coverage, regarding letting someone borrow your car, only applies to vehicles listed on your automobile policy.

In most cases, parents do not have to add their child to their auto policy as a driver until the child has a driver’s license.*

Coverage extends from your policy to the child until they can legally operate the vehicle unsupervised.

*Subject to state availability and guidelines

In general, any person who is or ever was licensed (in or out of the United States.) and lives in your household AND/OR regularly operates any of the vehicles listed on your policy, must be listed as a driver.*

While you must always list your spouse on you policy, you do not have to include other household members who have their own vehicle and insurance. A child away at college is considered a household member and must remain listed on your policy.

*Subject to state guidelines

No. Vehicles used for livery, including ridesharing services such as Uber and Lyft, are not eligible for coverage.

In most cases, “yes.” Electric Insurance will extend the broadest insurance of any vehicle on your auto policy to any private passenger type vehicle you rent in the United States, provided the rental period does not exceed 30 days.

Our insurance would apply as excess over any other collectible source of recovery (e.g., insurance provided by a rental company, travel or accident policies, or any applicable credit card coverage).

If you have purchased Collision and Other Than Collision/Comprehensive from Electric Insurance on one of your autos, that insurance will extend to insure damage to a rented vehicle, subject to your policy deductible.

For example, if the rental agreement provides a $1,000 Collision deductible and you have purchased from Electric Insurance a $250 Collision deductible, your policy with us will pay the difference between the $250 and $1,000.

If your Electric Insurance policy does not have Collision and Other Than Collision/Comprehensive coverage, you should consider purchasing the additional insurance from the rental agency.

Your Liability coverage (Bodily Injury, Property Damage) will also apply as additional insurance over and above the liability protection provided by the rental agreement.

Billing & Payments

Electric Insurance offers several convenient options for making payments.

- Sign into the MyAccount Policy Management Center to make a one-time payment or set up automatic, recurring payments from your checking or savings account or credit or debit card.

- Use the "ONE-TIME PAYMENT" button on the top menu of any page on our website.

- Pay by phone: Call our automated system any time at 844.516.4345.

- Pay by mail: Mail your check or money order to Electric Insurance Company, PO Box 9147, Chelsea MA 02150.

- Online banking (paying from your financial institution’s site): Be sure to enter your account number and the mailing address: P.O. Box 9147, Chelsea, MA 02150.

We have a range of payment plans, including monthly, quarterly, semiannual, and annual, to suit your needs. Installment fees apply and vary by state and payment plan. Payment-plan related discounts include the following options:

- Automatic, recurring payments can be used with any payment plan.

- The “Full Pay” plan rewards you for paying your full premium in a single payment. You’ll avoid up to $66 in service fees and may even get a 5% discount on your auto policy.*

- The semi-annual payment plan lets you pay your premium in two installments and earn a 3% discount on your auto policy.*

*Subject to state availability and guidelines

You must first select the annual payment plan (“Full Pay”) option in MyAccount. Please note that simply paying the full balance of your account will not trigger the system to apply the discount. Then make sure to check your most recent bill or contact Customer Service at 800.227.2757 to confirm your payment plan.

*Subject to state availability and guidelines

You can set up automatic payments in MyAccount by clicking “Pay My Bill” and choosing “Auto Pay.” This allows you to set up your account information from your checking/savings account or credit/debit card.

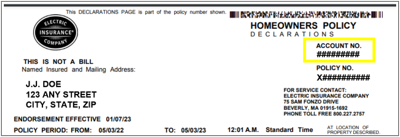

Your nine-digit billing account number can be found on any of the these Electric Insurance Company documents:

Your nine-digit billing account number can be found on any of the these Electric Insurance Company documents:

- Billing invoice

- Policy Declarations pages (see example)

- Vehicle ID cards

- Massachusetts Claims cards.

You can easily find your documents in the MyAccount Policy Management Center. If you have not yet enrolled in MyAccount, you can easily do so by following this enrollment link.

Electric Insurance accepts credit and debit cards (Visa®, Master Card®, American Express®, and Discover®), personal checks, and online banking payments. There are no additional fees for paying by credit card. If your check or e-check is declined for insufficient funds you will be charged a fee directly from Electric Insurance. Fees vary by state and range in amount from $15 - $25.

Payments may take 24-to-72 hours to be reflected on your account.

Any over-payment you make will be credited toward your next installment payment. If the account is paid in full, the amount will be refunded to you.

Late payments are subject to a late fee, as allowed by state regulations. If your payment is past due, you may be sent a Notice of Cancellation. If you receive a Notice of Cancellation for non-payment, please pay the amount due on the cancellation notice so that your policy will not be cancelled.

The option to pay premium through payroll deduction is available to employees of participating companies. If you are eligible, you can arrange to have your premiums deducted from your paycheck based on your pay schedule. Most participants receive 2% - 4% discount on your auto and home policies.* This is a convenient way to pay your premium without having to remember to pay bills!

*Availability and amount vary by state.

Auto Claims

Thanks for checking. Call us at any time at 800.227.2757 and follow the prompts to reach our auto glass claims team. We’ll help you find an in-network glass repair/replacement shop for any broken glass on your vehicle.

In-network claims are paid in full. If you use a facility outside of our network, you will have to pay the difference between the in-network coverage amount and the amount the out-of-network provider charges.

The provisions in your auto policy state that you must notify us promptly of an accident or loss (such as theft) involving your vehicle. Not reporting a loss in a timely manner could potentially affect whether coverage will apply to the loss.

All accidents and losses should be reported; a licensed adjuster will complete a full liability investigation to determine fault in the loss. Even if you are planning to file with the other party’s insurance company, you must still notify us so that we can complete a liability investigation.

Please do not call to report your claim from the scene of the accident—you may be distracted by police, tow trucks, or other involved parties. If any medical assistance is needed, call 911; otherwise, contact the police to report the incident. After making sure all vehicles involved are in a safe location, exchange needed information with any other parties involved, if possible. Key information includes:

- The name of each involved party’s insurance company and their policy number

- The names, contact numbers, and addresses of each driver involved

- The names, contact numbers, and addresses of any available witnesses

If it is safe to do so, take photos of the accident scene and all damages.

More tips on making an auto insurance claim

Knowing what not to do after an accident is just as important as knowing what you should do. There are 10 things you should keep in mind.

Should you file a police report? The answer is usually “yes.” Learn why filing an accident report with the police is a good idea.

If the police responded to the scene of an accident, then you may not need to make a separate report; however, if you are unsure, it is best to speak with the police department that has jurisdiction for the loss location.

If the police responded to the scene, you should obtain the department’s name and report number, if available, and provide these details to your adjuster. Your adjuster will request a copy of the police report. You can help speed the process by getting a copy of the report and sending it to us.

Learn why filing an accident report with the police is a good idea.

In general, coverage cannot be confirmed unless you file a claim. Coverage for a loss is determined by a licensed adjuster who is an employee of Electric Insurance Company.

Once the accident has been reported to Electric Insurance, an adjuster will contact you within 24 hours (one business day for Texas residents) to discuss your claim, applicable coverage, and next steps.

If coverage is available, a repair check will be issued within two days of receipt of the completed damage assessment. These timeframes exclude "Total Loss" vehicles and "Total Theft" of a vehicle.

How will my damages be assessed?

- In most states we can completed an initial repair estimate based on photos provided by you of the damage; your adjuster will provide instructions on where to text or email the photographs (Excludes MA and RI)

- You can also submit an estimate and photos from the shop of your choice

- In MA and RI a physical inspection by a licensed appraiser is required

However you choose to report your loss, online or via telephone, we need as much information as possible from you, including:

- The date, time, weather conditions, and location

- Statements from all parties involved (drivers, passengers, witnesses, etc.)

- Injury information

- Any involved party’s information (name, address, phone number, insurance information, etc.)

- The name of the responding police department and the report/case number

- Descriptions of the damage to the vehicle(s) and vehicle locations

Processing Your Claim

Throughout the life of your claim, we will make every effort to ensure a quick and stress-free a process for you as possible. Once your claim has been reported, your adjuster(s) will work with you to:

- Verify whether/what coverage applies to the loss based on your policy

- Take statements and gather information

- Evaluate all the facts and determine the cause of the accident

- Address any injuries sustained in the accident

- Assess the damage to your vehicle and issue payment accordingly

- Seek reimbursement of your deductible from any at-fault parties when applicable

Repairing Your Vehicle

Once you have an approved estimate and payment has been issued, you may schedule repairs with your body shop and provide it with a copy of the approved estimate (if they do not already have one). Scheduling is important so the shop can order and obtain the parts needed prior to when you drop the vehicle off. This ensures that once your vehicle goes to the shop, the repair process begins and limits the time you are without your vehicle.

Liability Investigation:

When it comes to “who is at fault,” it is not always as simple as “at fault” versus “not at fault.” The assigned adjuster will review all available evidence to determine to what extent each party contributed to causing the accident. Several factors are examined to determine fault, including, but not limited to:

- Driver and witness statements

- Police reports

- State laws

- General rules of the road

- Available video footage

- Damage photos

The policy deductible is the amount you chose to pay in the event of any loss, regardless of fault. The amount you selected when you purchased or renewed your auto policy can be found on the Declarations Page of your policy.

However, should you be found not at fault in the accident, we will make every effort to waive or recover your deductible from the at-fault party or their insurance carrier. The recovery process can take up to several months, depending on the circumstances of the event. Please note that there is never a guarantee of recovery. Recovery can be adversely affected by disputed liability, uninsured drivers, or many other resources.

When a policyholder is considered to be not-at-fault for an accident, Electric Insurance will make every attempt to reimburse the insured’s deductible as soon as possible. In most cases, the subrogation process occurs at the same time as the repair. The Subrogation Department will attempt to recover the insured’s deductible, vehicle repair costs, and covered rental expenses. In some states, medical expenses are included.

If a negotiated settlement is reached with the other insurance company for less than 100% (based on negligence), we will refund the deductible based on the percentage figure. Subrogation can be a lengthy process and may take an average of 60-120 days. Our representatives can explain this process to you in more detail if needed.

The first step to getting your vehicle back on the road is to estimate the damage to your vehicle. The fastest, most efficient way to do this is via a photo appraisal. Simply send us some photos of your vehicle via text or email. Once we have received them, one of our licensed appraisers will review the photos and prepare an initial repair estimate, typically within one business day of receipt.

If you are unable to submit photos yourself, we can send someone to photograph the damages for you.

If you have already obtained a repair estimate from a body shop, we can work with your shop directly to come to an agreed estimate.

Sometimes an in-person inspection is required, either due to state guidelines or the nature of the damage to your vehicle. In this case your adjuster will assign a licensed appraiser to schedule an inspection.

The initial estimate will be for the visible damage to your vehicle. Once your vehicle is in the body shop for repairs, should additional damage be found, we will work with your shop to address them.

If your vehicle is leased or under loan, the insurable interest of the loan/lease company must be protected as well; thus, any settlement checks for vehicle damage must be jointly issued to both you and the lien/leaseholder or to you and your body shop.

Repair shops will sometimes find additional damage to the vehicle after the original appraisal or estimate has been written. If so, the repair shop will notify Electric Insurance and send in a supplement estimate. As long as the additional damage is accident-related, it will be covered up to the approved amount.

Are you insured by Electric Insurance Company?

If you are, and your auto policy includes alternate transportation/rental reimbursement coverage, we will pay for your rental vehicle once your body shop begins repairs. Coverage will continue until either your vehicle is back on the road or until your coverage limit runs out, whichever comes first.

If your vehicle is a total loss, the amount of the authorized rental coverage may be limited, so you should begin shopping for a new vehicle once it’s been determined that it’s necessary to do so.

You can use any rental company you like; however, we do have contracted rates and a direct billing arrangement with Hertz as a convenience to you. That means that preferred (lower) rates would apply, making your coverage stretch a little further and that Hertz would bill us directly for the covered portion of the bill. If you do not have rental coverage on your Electric Insurance policy, and you are not at fault for the accident, you can seek reimbursement from the at-fault party’s insurance.

If you have a policy with Electric Insurance, the coverage on your own vehicle generally extends to the rental vehicle as well.

If You are not insured by Electric Insurance Company

Any reimbursement for a rental will be confirmed once the claim investigation is complete. Should Electric Insurance accept liability, your assigned adjuster will confirm the reimbursement rate and time-frame guidelines. Any rental vehicle obtained prior to a completed investigation will be considered an out-of-pocket cost with no guarantee of reimbursement by Electric Insurance.

Please note that Electric Insurance does not cover costs associated with gas, mileage, or any other optional insurance purchased with a rental vehicle.

Policyholders find contact information by:

Logging into the MyAccount Policy Management Center, or

Calling us at 800.227.2757 24/7/365.

Claim forms are sent to all parties involved in collision losses. In some states such as New York and California, state forms are also included in the mailing. These claim forms should be completed to the best of your ability. The driver of the vehicle should be sure to write down all details pertaining to the accident. For subrogation purposes, it is very important that we have the insured’s written report on file.

If you are insured with Electric Insurance or were a passenger in a vehicle we insure, you should report the loss to us and we will assign an adjuster. This adjuster will review your policy for available coverage for things such as medical bills and/or lost wages.

First-party injury coverage varies depending on the state in which your policy is written. If your policy contains first-party injury coverage, you should see the physician of your choice. Provide the physician’s office with your claim number, and your adjuster’s name, phone number, fax number, email address. Make sure to include Electric Insurance’s address (75 Sam Fonzo Drive, Beverly, MA 01915) as well.

If, during the claim process, you are sent any bills from your medical providers, please forward them to your adjuster.

If the other driver is determined to be at fault for the loss, contact their insurance company to inform it that you are injured and discuss with them their process for a Bodily Injury claim for your injury damages. This includes any pain and suffering damages.

If you were involved in an accident with someone insured by Electric Insurance and are injured, report the loss to us. An adjuster will be assigned to you and will review the claim process. Bodily Injury coverage is ultimately a liability coverage; thus, it is not considered primary for medical expenses, and typically, first-party coverage from your own auto insurance or health insurance would be primary for billing.

New Jersey Personal Injury Protection Provider Information

The documents below provide information about Electric Insurance Company’s New Jersey Decision Point Review Plan as required by the New Jersey Department of Banking and Insurance. New Jersey has established a course of treatment for automobile-related injuries and includes a list of approved providers for EMG (Electromyography) and diagnostic testing.

Description

- Notice to Patient (PDF 81kb) State-approved Decision Point Review Plan for the patient

- Notice to Provider (PDF 80kb) State-approved Decision Point Review Plan for the provider

- Attending Provider Treatment Form (PDF 40kb) Blank Attending Provider Treatment Plan for the provider

- Mandatory Internal Appeal Forms (PDF 60kb) Blank Pre-Service and Post-Service Appeal forms for providers

A vehicle is deemed a total loss in most states if the estimated repair cost of your vehicle exceeds the value of your vehicle, rather than whether your vehicle can be repaired.

However, there are varying statutes related to determining a total loss. In each case, our licensed appraisal team reviews and applies the state-specific guidelines when assessing damages. Vehicle damage must be assessed by a licensed appraiser to confirm whether your vehicle is a total loss.

If the damage to your vehicle is confirmed to be a total loss, an adjuster who specializes in “total loss” claims will work with you to settle your claim. After we obtain a market valuation of your vehicle, we will calculate the settlement amount and send you documentation outlining the settlement and the documentation we require from you (such as the title, odometer statement, etc.) based on state guidelines to complete your claim. Payment for your claim will be issued once all requirements have been met. If your totaled vehicle is at a tow yard or body shop, you should remove any personal belongings from it. Based on your state, your adjuster may instruct you to remove the license plates. You must also inform the tow yard or body shop that Electric Insurance is permitted to pick up the vehicle and move it to a facility that does not charge storage fees.

Once a settlement amount is agreed upon, the total loss adjuster will also advise you how much longer an authorized rental car will be covered.

If there is a loan on your vehicle, we have to speak to the loan company and obtain the loan payoff amount and documentation. If the settlement amount exceeds the balance of the loan, you as the vehicle owner will be issued a check for the difference between the settlement and loan amount. If the settlement amount is less than the loan payoff amount, then the entire settlement amount is issued to the loan company and the remaining loan amount is handled directly between you and the loan company.

If any loan or insurance payments are due on the vehicle during the total loss claim process, it is in your best interest to keep up with your payments. Once the claim process is complete, policies and loans are typically adjusted retroactively based on when the loss occurred. You don’t want to incur any potential penalties that may come with late payments.

Most states have specific rules when it comes to whether you can retain and repair your vehicle. Your total loss adjuster will be able to review the requirements associated with retaining your vehicle. If you are able to retain your vehicle, your settlement will generally be less than it would if you did not retain your vehicle. This is because the salvage value and sometimes other items are usually deducted when calculating the settlement figures. To better understand your options, talk to your adjuster to go over the specific resources that may affect the settlement of your claim.

Claim terminology may be difficult to understand. Here's a glossary of auto claim terms that explains the most common.

Discounts

Electric Insurance offers a variety of auto insurance discounts that can help save you money on your auto and home insurance. Discount availability and amounts vary by state and include:

- New customer "Plan Ahead" discount - up to 15%

- Multi-policy discounts of up to 10% on your auto policy and up to 25% on your home policy when you insure both your vehicles and home with us.

- ABS brakes, airbag, anti-theft, and daytime running lights

- Electric and hybrid vehicles

- Employees of participating businesses

- Good student credits

- Mature Driver and Teen Driver training course completion

- Multi-vehicle credits

- New and newer vehicles

We offer a wide range of discounts for home, condo and renters policies: multi-policy discounts, the "Welcome!" discount for new home coverage customers, safety and anti-theft device discounts and more. Please note that discount requirements, availability and amounts vary by state.

General Topics

- FL – 01976

- MA – 309

- NY – 463

- All other states – 21261

Electric Insurance has been providing high-quality auto, home, and umbrella insurance since 1966, when we were founded to provide benefits for employees of the General Electric Company. We now provide the same exceptional products and services to employees of hundreds of large businesses nationwide and to the general public.

Insurance companies use credit-based information to evaluate insurance risks and determine a consumer’s pattern of credit management. Some credit factors taken into account are payment history, public records such as bankruptcies or judgments, outstanding debt, and length of credit history scores. It has been statistically proven that the higher the credit score, the better the insurance risk.

Individuals with favorable credit history generally file fewer and/or less expensive claims. Using credit to supplement the underwriting process allows Electric Insurance to make precise underwriting decisions. This results in more competitive, affordable rates for you. Please note: Use of insurance scores is not applicable in all states.

AM Best, one of the insurance industry’s top financial rating agencies, has given Electric Insurance ratings of “A/Excellent."

An Umbrella policy is a valuable part of an individual’s or family's personal insurance plan. It provides additional financial protection when a claim or judgment against you exceeds the amount your auto, home, boat or other insurance liability coverage.

Yes! We strongly encourage you to get electronic copies of your policy documents.

Simply enroll in our eDocument Delivery Program to have your policy documents emailed to you as easy-to store and retrieve email attachments. If you must file a claim, you’ll have quick access to your coverage information – even if a catastrophe has destroyed your home and the paper files in it. Use the link below to send an enrollment request email to our Customer Service team. They’ll take care of the rest.

Please note that any applicable cancellation notices will be sent through the United States Postal Service as required by state law.

Home, Condo, and Renters Insurance

Get insurance for your home that covers more than just the structure. Our homeowners policies cover your house, the belongings in it, your garage, shed, fence, pool, and any other buildings on your property. They even include liability coverage to protect you from lawsuits. So, if a guest is accidentally injured, you’re covered. If you can’t live in your house because it’s too badly damaged by something your policy covers, we’ll even pay your additional temporary living expenses.

Your condo’s master policy only covers so much. You need a condominium unit owners insurance policy that covers everything from the interior of your unit to your furniture, cabinets, appliances and personal possessions. It should even cover you for liability issues if someone is hurt in your unit. Our condo policies do all that and a lot more.

You may not own your living area , but you do own your belongings. You’ll want to protect them from fire, theft, vandalism and a whole lot of other ways they could be stolen damaged, or destroyed. You also need to protect yourself from liability claims against you. Remember, if your guest trips on your rug and ends up in the Emergency Room of the hospital, it’s not your landlord who has to pay the damages.

In most cases, your homeowners (or condominium unit owners or renters) policy would extend to cover your child’s property in a dorm or other residence if the student is under age 24, enrolled in school full-time, and was a resident of your household before moving out to attend school.

The coverage amount is limited to 10% of your policy’s Coverage C amount or $1,000, whichever is greater. The coverage applies to personal property anywhere in the world if the loss was caused by a covered peril. The policy deductible would apply.

You may wish to consider a separate renter’s policy for your child. If your child makes a claim under the renter’s policy, it would not adversely affect your home policy (such as removing any “claim-free” discount or adding a surcharge to your premium.) Please note that a landlord may require all renters to have a renter’s policy.

Yes! We strongly encourage you to get electronic copies of your policy documents.

Simply enroll in our eDocument Delivery Program to have your policy documents emailed to you as easy-to store and retrieve email attachments. If you must file a claim, you’ll have quick access to your coverage information – even if a catastrophe has destroyed your home and the paper files in it.

Use the link below to send an enrollment request email to our Customer Service team. They’ll take care of the rest.

Please note that any applicable cancellation notices will be sent through the United States Postal Service as required by state law.

Home Insurance Property Claims

Yes. Based on the provisions of your home policy, you must notify us promptly of any accident or loss (e.g., theft) involving your home. Not reporting a loss timely could potentially impact whether coverage will apply for the loss.

While it is best to have as much information as possible regarding the loss as is available when you report a claim, keep in mind that you should report the loss as soon as possible, regardless of how much information you have.

The following information is not required to start your claim but will eventually be needed.

Information on all parties involved, the date of loss, the cause of loss, any injuries, and/or damage to any structures on your property or their contents.

A copy of your association’s bylaws if you own a condominium unit.

A copy of your lease agreement if you are a landlord or renter.

If you report a claim online, a licensed adjuster will follow up with you to gather any needed information that is not included in the initial report.

The licensed adjuster to whom you reported the accident will usually generally investigate and process your claim. If your claim must be assigned to another adjuster, that person will contact you as quickly as possible.

If the police responded to the incident, you may not have to make a separate report; however, if you are unsure, it is best to speak with the police department that has jurisdiction for your property’s location.

If the police responded, you should obtain the department’s name and the incident report number, if available, and provide these details to your adjuster. Your adjuster will request a copy of the police report as needed. You can help speed the process by getting a copy of the report and sending it to us.

Police reports are commonly requested by claims adjusters in order to verify the occurrence of a claimed theft or vandalism loss. Reporting the loss to the police and us as promptly as possible is the best way to prevent coverage issues and ensure your claim is processed as quickly as possible.

If your home has a loan or lien on it, the insurable interest of the loan/lienholder must be protected as well; thus, any settlement checks for damage to the structure will need to be jointly issued to you and the mortgage company/lien holder.

In almost all cases, your deductible does apply to a home loss. The deductible amount can be found on the Declarations Page of your policy.

The most likely cause is the depreciation applied to the value of your property. Depreciation is commonly defined as a reduction in the value of an asset over the passage of time. In the case of homeowner’s insurance, depreciation can be “recoverable” or “non-recoverable” and is based on the age and condition of the property at the time of the loss.

“Recoverable” depreciation is the amount held back at the time of initial claim payment and paid once repairs are completed or the applicable item(s) has otherwise been replaced. “Non-recoverable” depreciation is not paid back at the time repairs have been made or the applicable item(s) has been replaced.

Get yourself and your fellow residents to safety. Your safety should always be the top priority.

- Notify us of the loss as soon as possible. We have staff available 24/7 to help with immediate, emergency needs, such as contacting a mitigation company on your behalf or finding you temporary accommodations if your home is no longer habitable. We can also guide you through the claims process and guide you from taking any actions that could negatively impact the outcome of your claim.

- Prevent further damage by contacting a professional mitigation company. Mitigation companies are available nationwide to assist with emergency services such as water cleanup, fire remediation, or boarding up a structure damaged by a fallen tree.

- Document the damage and the costs you incur. Taking photographs of the damage prior to any emergency services being completed is highly recommended, as those photographs may be the only available documentation to show what the property looked like prior to the emergency service taking place. Keep all receipts related to your claim-related costs. Many of the costs you incur may be reimbursable if they were needed to prevent further damage to your home or were additional expenses you incurred due to a covered loss.

“Additional Living Expense” is a common coverage included in most homeowners’ policies. It covers the cost of temporary accommodations needed due to a covered claim event that makes your home uninhabitable.

Contact the Claims Department and request assistance if you must secure temporary accommodations, as we can assist in rapidly locating a place for you to stay using our vendor, ALE Solutions.

We actively monitor major fires, windstorms, hailstorms, tornadoes, hurricanes, and other natural and unnatural events across the country daily. In the event of a significant event, our Catastrophe Response Team may be dispatched to your area to assist.

The team checks in on our customers while they are in a catastrophe area, whether or not they have placed a claim, so do not be surprised if you find one of our team members knocking on your door shortly after an event!

We may use satellite imagery and/or drone technology to inspect damage your home. These newer tools have greatly increased our capacity to quickly and accurately assess damage to your home, which means we can process your claim much more quickly.

If you experience a loss, report it to our office promptly and we will dispatch one of our adjusters to your home right away.

Flood damage is NOT covered under a homeowners’ policy. Only flood insurance protects your home against rising water, mudflow, overflow of inland or tidal waters, and local drainage problems. Everyone is in a flood zone, whether high risk or low-moderate risk. Homeowners whose properties are located in high-risk zones will be required by their mortgage company to obtain flood insurance.

About 20 percent of all flood losses reported are from low-to-moderate risk areas. Electric Insurance places flood insurance policies through Wright National Flood Insurance Company. Electric Insurance acts as the customer’s agent for flood insurance. Coverage is limited to certain specific Building Coverage and Contents elements.

Learn more about the ins-and-outs of Flood Insurance coverage.

When you review your homeowners, condo, or renter’s policy, you will see multiple sections of coverage. It’s important to understand these, and the definitions and exclusions in the policy. Follow this link for a high-level summary of coverages.

If you suffer any loss or damage to your home, you should contact us to file a claim as soon as it is safe to do so, either by filing the claim online or via the telephone. Not reporting a loss in a timely fashion could potentially affect whether coverage will apply for the loss.

You will be asked to provide detailed information about the loss, such as the parties involved, the date of the loss, the cause of the loss, and the damage you are claiming in order to establish a claim. Once the claim has been established, a licensed adjuster will be assigned to investigate your claim and review the policy to verify whether/what coverage applies. A written repair estimate for the damages will be needed. It can be written by one of our licensed claim adjusters based on photos and information you provide, or we may have an independent adjuster assigned to inspect the damages in person. Depending on the circumstances of your loss, the adjuster handling the claim may also request an estimate from your contractor.

Tips for expediting the process

- Have as much information available as possible regarding the loss when you report the claim.

- If you are a condo owner, please make a copy of your association’s bylaws available to us.

- If you are a renter or a landlord, please make a copy of your lease agreement available to us.

If you are reporting the claim online, a licensed adjuster will follow up with you to gather any missing information not included in the initial report.

If you already have an estimate from a contractor, we can work with the company directly to come to an agreed scope and price for the repairs. Depending on the circumstances of your loss, an independent adjuster, or other similar expert, may be assigned to inspect your home and generate an estimate on our behalf. However ,the estimate is generated, it will generally be for only the visible damage.

In the event your preferred contractor finds additional damages that were not included in the initial estimate or does not agree with the pricing of our estimate, we will work with the company to address the additional damages and/or costs.

Please notify our office of any increased cost or additional damages before starting that work so we may make sure they are covered and Electric Insurance agrees to the additional cost of the repair.

We understand that there’s a lot of unfamiliar terms related to home insurance claims. This glossary will help you understand some of the most common.

In most cases, your homeowners (or condominium unit owners or renters) policy would extend to cover your child’s property in a dorm or other residence if the student is under age 24, enrolled in school full-time, and was a resident of your household before moving out to attend school.

The coverage amount is limited to 10% of your policy’s Coverage C amount or $1,000, whichever is greater. The coverage applies to personal property anywhere in the world if the loss was caused by a covered peril. The policy deductible would apply.

You may wish to consider a separate renter’s policy for your child. If your child makes a claim under the renter’s policy, it would not adversely affect your home policy (such as removing any “claim-free” discount or adding a surcharge to your premium.) Please note that a landlord may require all renters to have a renter’s policy.

MyAccount Policy Management Center

You can do quite a bit! Here's a high-level list of the most popular features with links to "how-to" videos:

- View and/or download your auto insurance ID cards

- Set up automatic payments

- Add a driver to or remove a driver from your auto policy

- Add or remove a vehicle to/from your auto policy*

- View/print policy documents

- Update contact information

*Please note vehicles cannot be added or removed from a Massachusetts, policy, and cannot be removed from a New York policy.

Massachusetts Registered Auto Repair Shops

While our Massachusetts policyholders are free to use the auto repair shop of their choice, our network registered repair facilities will guarantee their work for as long as you own your vehicle.

New Jersey Personal Injury Protection

The documents below provide information about Electric Insurance Company’s New Jersey Decision Point Review Plan as required by the New Jersey Department of Banking and Insurance. New Jersey has established a course of treatment for automobile-related injuries and includes a list of approved providers for EMG and Diagnostic Testing.

Description

Notice to Patient (PDF 81kb) State-approved Decision Point Review Plan for the patient

Notice to Provider (PDF 80kb) State-approved Decision Point Review Plan for the provider

Attending Provider Treatment Form (PDF 40kb) Blank Attending Provider Treatment Plan for the provider

Mandatory Internal Appeal Forms (PDF 60kb) Blank Pre-Service and Post-Service Appeal Forms for Providers

Roadside Assistance Service Claims

Our Roadside Assistance Services are included with Towing and Labor coverage. They are for situations where you require roadside assistance for a reason other than an accident or a loss under Comprehensive Coverage. Some examples of applicable losses are:

- Mechanical breakdown

- Flat tire changes using your spare

- Jumpstarting a dead battery

- Vehicle lockout

Call our Roadside Assistance Services line 24/7/365 at 800.578.3543 if you need assistance.

If you have already used roadside assistance services and are seeking reimbursement under your policy's coverage, please send us the invoice at Claims@ElectricInsurance.com for review/reimbursement. Please be sure to reference your policy number in the subject line. Once we receive your invoice, we either will issue payment or reach out to you if there are any coverage-related questions.

Please note, if you require assistance as the result of an accident, towing services would be covered by Collision Coverage, if your policy includes this coverage. To arrange a loss-related tow, please call us at 800.227.2757 and follow the menu prompts to speak with a representative who will review your coverages and outline the steps needed to arrange a tow and the process for reimbursement if your policy includes coverage for towing.