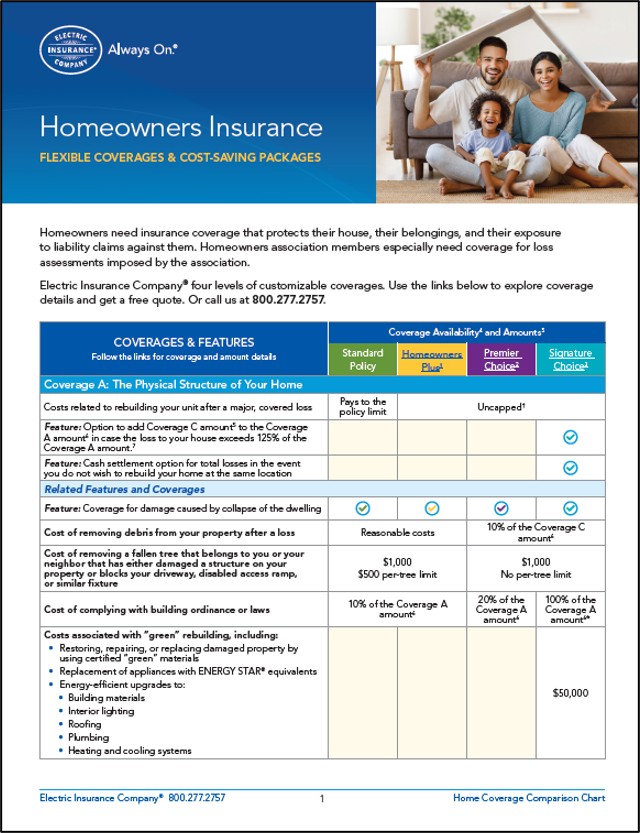

Homeowners Plus

Homeowners Plus

Eight more coverages and six higher coverage amounts than a standard policy

Standard homeowners insurance provides limited coverage, generally offers low coverage amounts, and requires you to purchase separate endorsements (riders) to add important coverages and features.

Homeowners Plus does better than that. It adds coverage for two favorable claim payment types, plus four additional coverages and six higher coverage amounts than a standard policy.

Four Key Coverages Upgrades

Payment for rebuilding your home after a major loss

Payment for replacing your damaged or destroyed personal property with new items

Payment towards cleaning/repairs if your water or sewer pipe backs up into your house, or if your sump pump fails.

Liability coverage for claims and lawsuits against you

Great for Etsy, Small eBay, Shopify Sellers and Occasional Freelancers

Coverage for your incidental business

Coverage for loss to your business data

Coverage for loss to your business property

Safety & Security Reimbursements

Reimbursement for replacing your door locks

Reimbursement for fire department service charges

Coverage for spoilage of refrigerated/frozen foods

Higher Coverage Amounts

Payment for theft of money from your household

Payment for loss costs related to credit cards, EFT cards/access devices, and more .

Payment for theft and/or disappearance of jewelry, precious/semi-precious stones, watches, and furs

Payment for theft and/or disappearance of silverware and other valuable metal ware

Payment for reimbursing another person if you accidentally damage their property

Coverage for HOA Member Assessments

HOA members have their fair share of fees, including charges (assessments) related to repair or replacement of damage done to common areas of the association. If your HOA assesses you a fee related to a loss, such as repairs for damage to a tennis court that was damaged when a tree fell on it, this coverage would pay up to $1,000.

Homeowners Need a Risk Coach™

A 2022 insurance survey found that 96% of respondents misunderstood at least one important feature of their coverage. More than half misunderstood several features. We want better than that for our clients. So our Risk Coach consultants are licensed insurance professionals who are trained to look at coverage from your perspective. They help ensure you get the right coverage at the best price.

Home values are at an all-time high. Make sure you protect your investment in your home with sound coverage. This easy-to-understand coverage chart (PDF 820kb) helps you know what to get and why.

Utility Line Repair and Replacement coverage. Municipalities and utility company often place the burden - and cost - of repairing or replacing damaged service lines. This very inexpensive ($66 per policy term) endorsement provides up to $20,000 in coverage.