Standard Condo Unit Insurance

Condos are great. You get many of the benefits of homeownership, usually at a lower cost and reduced level of upkeep. You even get to share some of the expenses — and risks — with your fellow owners.

But some things are entirely your responsibility. You must protect your personal belongings and your liability for people getting hurt — and even the building materials used to finish your unit.

Condo Unit Coverages

Condo Owners Association Loss Assessment cost

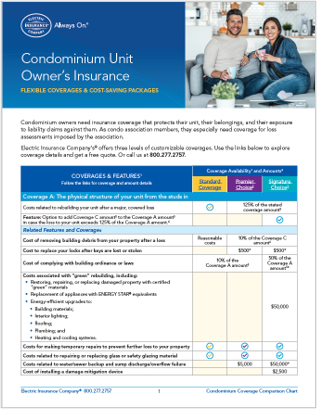

Coverage A: The physical structure of your unit and permanent furnishings

Coverage C: Your personal belongings

Coverage D: Additional living expenses

Coverage E: Personal Liability

Coverage F: Medical payments to others

Additional Coverages

Reimbursement for compliance with a building ordinance or law.

Reimbursement for fire department service charges

Coverage for grave markers and mausoleums

Costs related to removal of debris and trees

Payment for damage to or loss of trees, shrubs, and other plants

Coverage for electronics in/on a motor vehicle

Coverage for Specialty Items and Circumstances

Payment for loss costs related to credit cards, EFT cards/access devices, and more

Theft of money and precious metals from your household

Theft of firearms and related equipment

Theft of jewelry, precious/semiprecious stones, watches, and furs

Theft of silverware and other valuable metal ware

Valuable papers and securities

Payment for reimbursing another person if you accidentally damage their property

Watercraft and utility trailers

For Etsy, Small eBay, or Shopify Sellers and Occasional Freelancers

Coverage for your incidental business

Coverage for loss to your business property

Five Things That Could Be Better

A standard condo policy provides basic coverage only and has what we call “gaps and gotchas.” Here are a few of the biggest:

Limited condo owners association loss assessment coverage

Depreciation applied to claim payments

Low coverage amount for your belongings

Limited coverage for your small valuables

Narrow coverage for for claims and lawsuits against you

Customize Your Policy

Youi can tailor our condominium unit owners policies with customized coverage amounts and endorsements. You can get coverage that meets your needs without being charged for coverage that doesn’t.

Take the Risk Coach™ Approach

A 2022 survey found that 96% of survey respondents misunderstood at least one important feature of their insurance coverage. More than half misunderstood several. We want better than that for our clients. When you work with our Risk Coaches, you’ll work with a licensed insurance professional who’ll help you get the right coverage at the best price.

Need More Than the Basics?

If you need more than the basic coverages and coverage amounts outlined above, check into our Premier Choice Condo (includes 13 more coverages and 18 higher coverage amounts) and Signature Choice Condo (best for high-value units) options.

These coverage packages include more coverages and higher coverage limits. Packages offer more advanced coverages at lower rates than adding them as separate endorsements. Take a quick look at this handy coverage comparison chart.