Share this:

Call or Use Chat to Contact a Risk Coach

For a no-cost and no-obligation-to-buy coverage-needs assessment, use the chat feature on this page or call us at the number below. Our Risk Coaches are glad to help you get the coverage you need for your home.

Call us at 800.342.5342, Monday through Friday, from 8:00 a.m. to 8:00 p.m. ET.

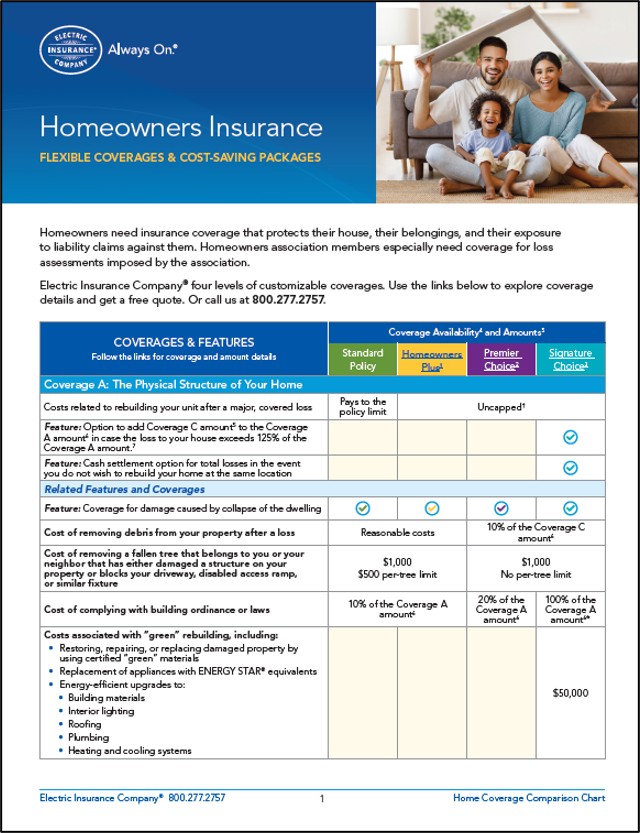

Home values are at an all-time high. Make sure you protect your investment in your home with sound coverage. This easy-to-understand coverage chart (PDF 820kb) helps you know what to get and why.